The Roundup by TSG Consumer - Issue #22

A bi-weekly roundup of the latest news and opinions across brand building, consumer companies, and consumer trends from TSG Consumer.

TSG Consumer is a leading private equity firm, and trusted partner in building brands people love since 1986.

What you can expect from this newsletter

A bi-weekly round-up of all things consumer. This is a space for people from across the consumer space to stay up to-date on the latest trends, connect with like-minded peers, and continuously learn from each other

Each issue will feature a curated selection of recent consumer headlines - stay tuned for insights that keep you up to speed in the ever-evolving consumer space!

The Roundup:

An Investor’s Guide to Gen Alpha (Josyana Joshua and Dina Katgara, Bloomberg): Gen Alpha (born 2010-2024) is roughly 2 billion people strong globally, already commands more than $100 billion in annual U.S. direct spending power, and is forming financial habits earlier than any prior generation thanks to native access to digital commerce. Bloomberg highlights five trends shaping where that money goes:

AI native. 64% of teens use AI chatbots, per Pew. For Gen Alpha, AI isn’t a tool they adopted later in life; it’s a interface for school, content creation, and search.

Gaming as a social network. 85% of U.S. teens play video games. Roblox, Fortnite, and Discord have joined, if not supplemented, Instagram and Facebook as the primary social layer. Gen Alpha communicates while playing, not while scrolling. That said, gaming broadly is facing pressure: legalization of sports betting and prediction markets, plus a macro battle for attention against short-form content, are all weighing on engagement.

Wellness from birth. 59% of Gen Alpha cite mental health as a top concern. Therapy platform Headway logged 650,000 appointments from Gen Alpha users last year.

Resale is mainstream. The global secondhand market is projected to reach $360 billion by 2030, growing 10% annually, per BCG. This cohort treats vintage as a feature, not a compromise.

Physical retail is back. 66% of Gen Alpha shoppers prefer buying in-store, and just 3% would rather shop exclusively online, per Numerator. AMC is leaning in with themed merchandise drops, while retailers like Ralph Lauren are expanding in-store cafés to extend dwell time.

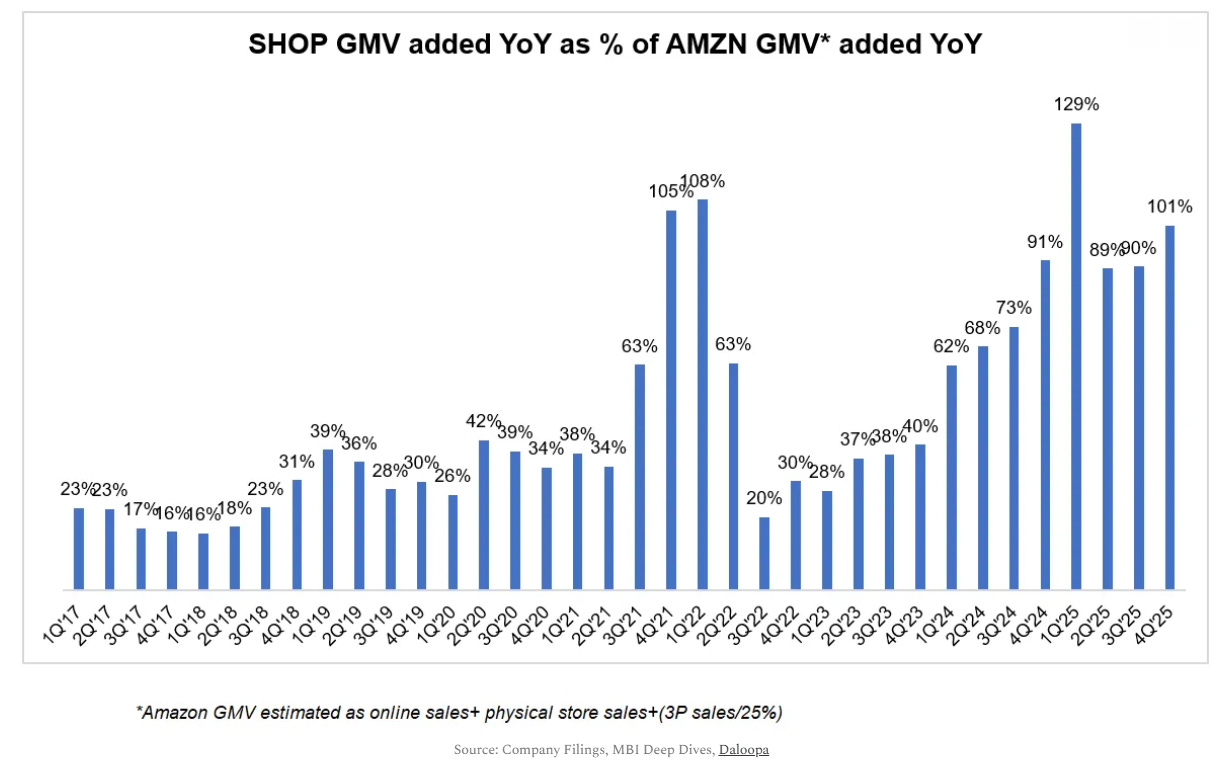

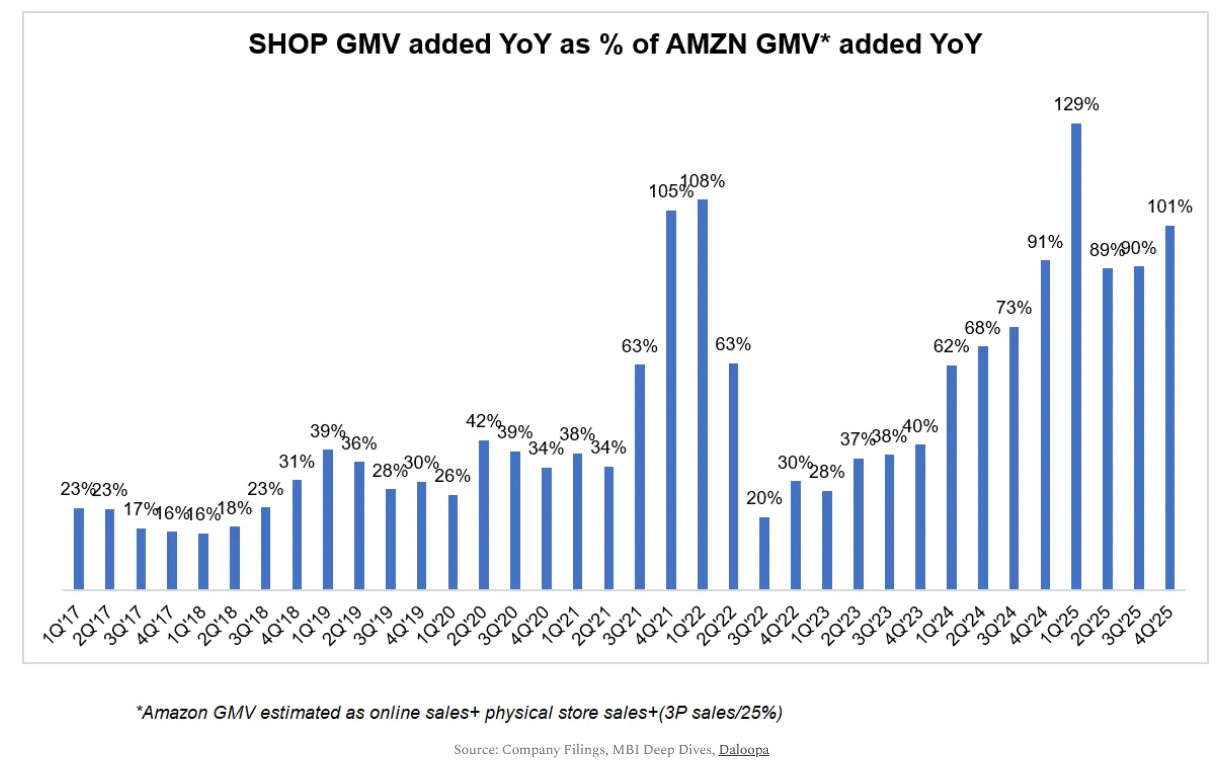

Shopify and the SaaS Panic (Ben Thompson, Stratechery): Shopify posted Q4 revenue of $3.7 billion (up 31% YoY) and $124 billion in gross merchandise volume, both beating estimates. The stock fell 13% after adjusted EPS of $0.48 missing consensus expectations of $0.51. This feels like a SaaSpocalypse panic in miniature: the market is treating every software company as an AI casualty, regardless of whether AI is a headwind or a tailwind. As Ben Thompson eloquently argued on Stratechery last week, Shopify’s logic should run in the opposite direction. Shopify sits atop trillions of data points from billions of transactions across millions of merchants, and it’s deploying that data through Shop Campaigns, a new Product Network that cross-sells inventory across Shopify stores, and the Universal Commerce Protocol co-developed with Google to power agentic commerce.

Anyone who has used Shopify knows that it does far more than build storefronts. It runs checkout, payments, taxes, shipping, fraud prevention, and fulfillment. That full-stack coverage is exactly what makes Shopify hard to displace and easy to layer AI on top of. When an AI agent surfaces a product for a consumer, someone still has to process the payment, ship the box, and handle the return.

Orders from AI search to Shopify stores are up 15x since January 2025 (off a small base). Thompson’s broader point is that AI-driven commerce will favor the long tail of merchants, which is Shopify’s core constituency. Shopify now represents over 14% of U.S. e-commerce. To anyone running a business on Shopify, this sell-off smells like pattern-matching gone wrong: Shopify got lumped in with software companies AI threatens, when it’s likely one of the platforms AI makes more valuable.

Waymo’s $126B Fundraise (Om Mallick, On My Om): Waymo closed a $16 billion round ($13 billion of it from parent Alphabet) at a $126 billion valuation, roughly 360x its ~$350 million annualized revenue run rate. For context, Uber trades at 3-4x revenue. Om Malik digs into the physics of the business, and the numbers are stubborn. Waymo’s ~2,500 Jaguar I-PACEs average about 25 trips per day and already operate ~16 hours daily. To reach its target of one million weekly rides by the end of 2026, the fleet would need to more than double to 5,500-6,000 vehicles, at roughly $175,000 per car, which is over $600 million in vehicle costs alone. New city launches offer limited near-term relief. Austin, nine months in, accounts for just 8% of rides with roughly 200 vehicles. The valuation debate echoes the famous 2014 exchange between Aswath Damodaran and Bill Gurley over Uber. Damodaran sized Uber against the existing taxi and limo market and arrived at a modest valuation. Gurley argued that Uber would expand the market by making rides cheaper, faster, and more accessible than car ownership in many contexts, and he was right. Valuing Waymo requires a similar leap: that autonomous vehicles don’t merely substitute for rideshare trips, but create entirely new demand by being cheaper (no driver), safer, and available 24/7. The obvious downside is that, unlike Uber’s asset-light model, Waymo’s growth is constrained by atoms, not bits. Every incremental ride requires a physical car, a mapped city, regulatory approval, and charging infrastructure. Both sides of that argument deserve serious consideration.

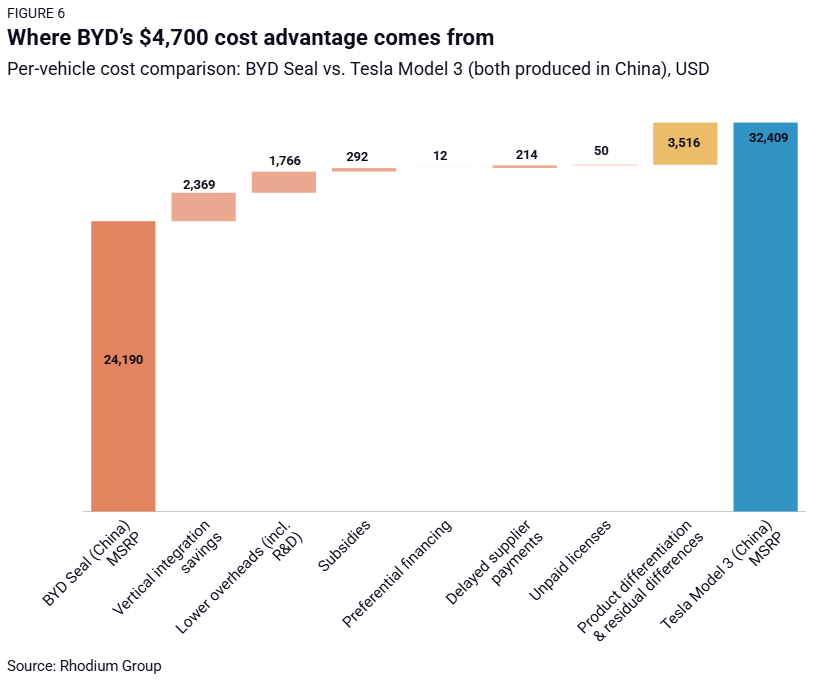

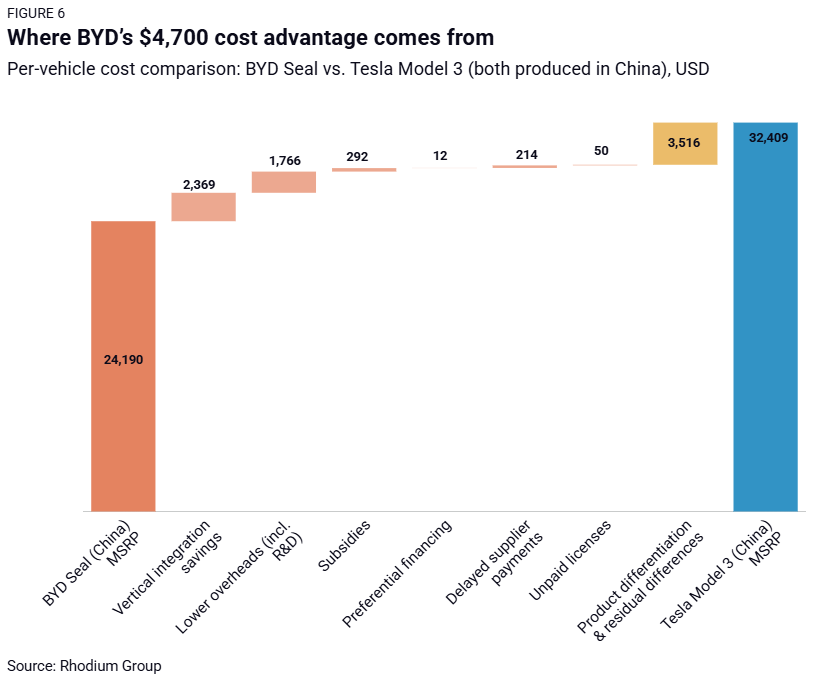

Why Are Chinese EVs So Cheap? (Gregor Williams, Rhodium Group): The conventional explanation for Chinese EV pricing points to subsidies and cheap labor. Rhodium Group's cost analysis tells a different story. Comparing BYD's Seal to Tesla's Model 3 (both produced in China), BYD enjoys a roughly $4,700 per-vehicle cost advantage, about 15% of the Model 3's sticker price. Subsidies explain just 5% of that gap (~$292 per vehicle). Labor productivity actually favors Tesla, which generates six to seven times more revenue per employee than BYD.

The real advantage is vertical integration. BYD manufactures far more components in-house, avoiding supplier markups worth an estimated $2,369 per vehicle relative to Tesla. The second largest factor is lower overhead per vehicle ($1,766 advantage), largely due to concentrating R&D in China.

So where does this leave U.S. automakers? In January, Ford CEO Jim Farley pitched the Trump administration on allowing Chinese EV makers to manufacture in the U.S. through joint ventures where American firms retain controlling stakes. Bloomberg described this as a mirror image of China’s own requirements decades ago, when GM, VW, and Toyota needed local partners to access the Chinese market. The proposal was rebuffed, but the logic is hard to ignore. Ford already licenses CATL's battery technology (CATL is a Chinese battery manufacturer) for a $2-3 billion plant in Michigan. GM is importing CATL cells for the new Chevy Bolt. Ford is reportedly in talks with Geely (a Chinese auto group) on manufacturing partnerships. Canada isn't waiting around: in January it cut Chinese EV tariffs from 100% to 6.1%, contingent on joint ventures with Canadian firms within three years. The cost gap Rhodium identifies is structural, not temporary. Western automakers must decide whether to replicate these advantages through partnerships, or simply cede the ground.

Quick Hits:

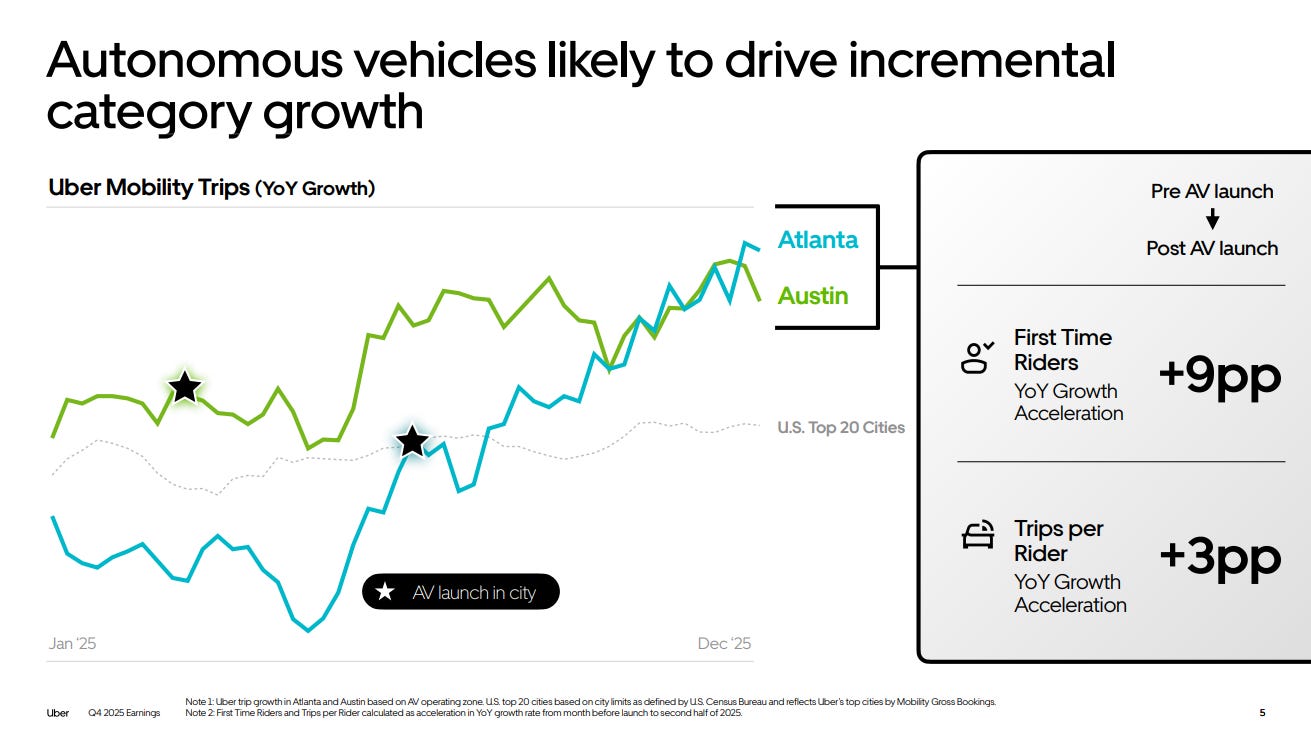

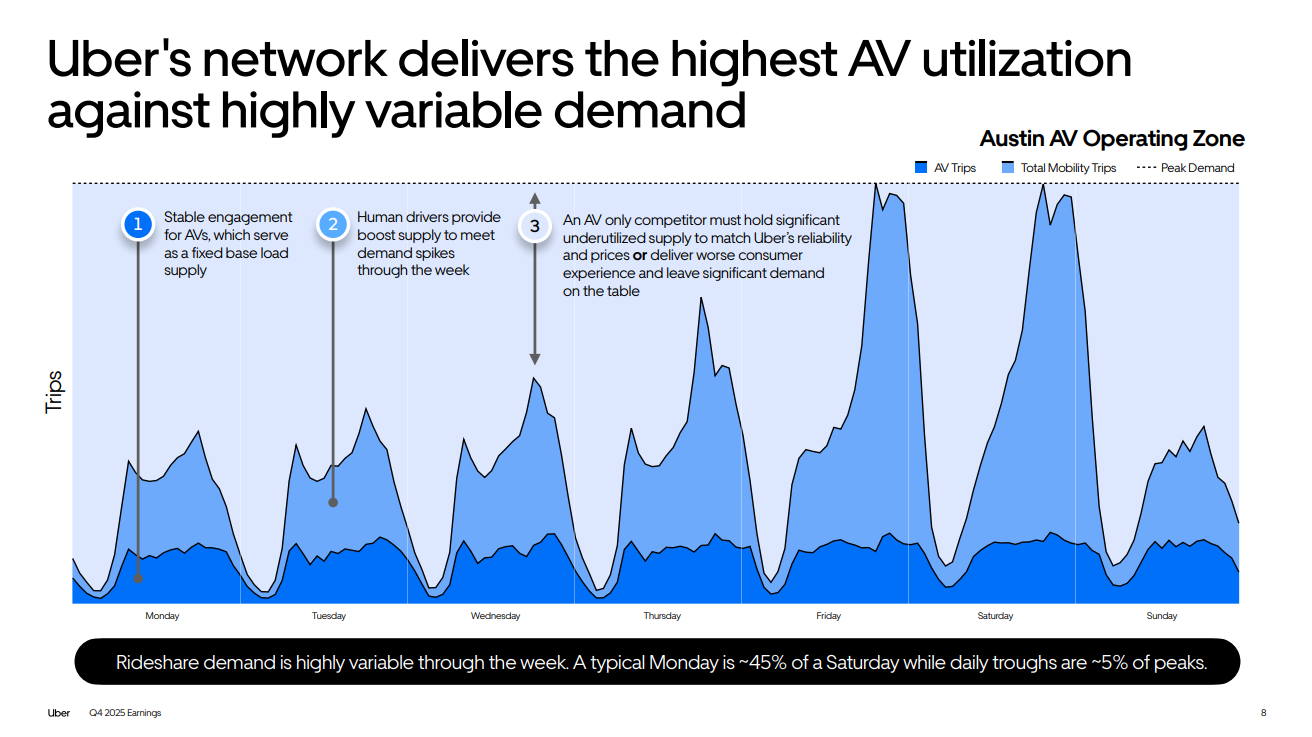

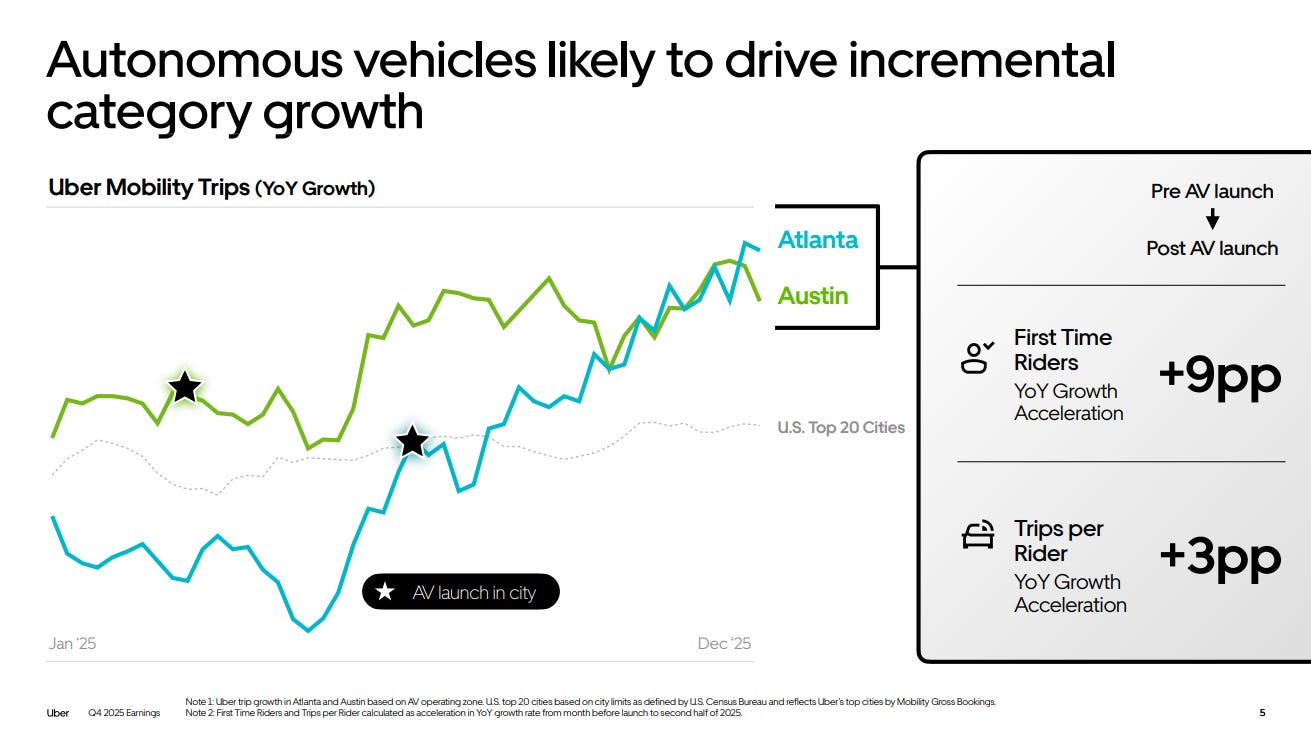

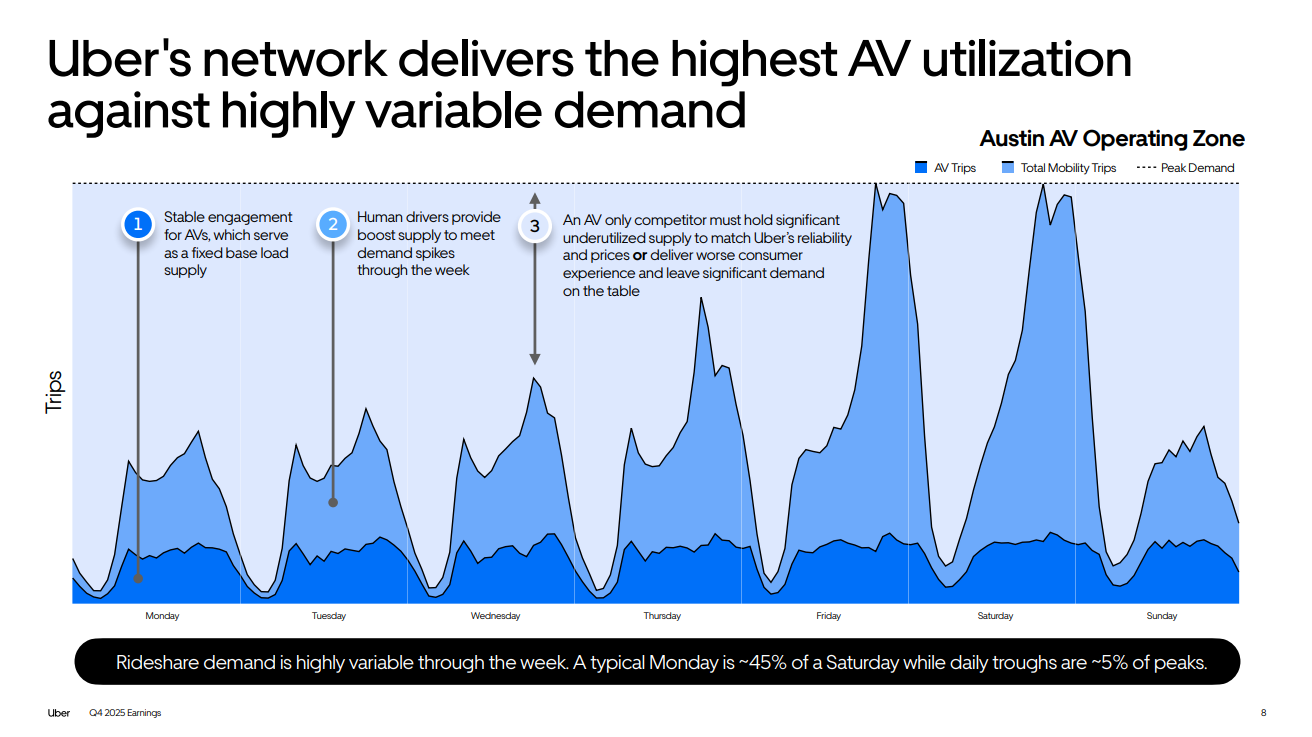

From Uber’s Q4 Earnings: Uber shared early data showing that AV launches accelerated overall usage, particularly among first-time riders, evidence that autonomy is expanding the category. AVs complete 30% more rides per day and arrive 25% faster than human drivers. One open question: given highly variable demand, will it make sense for AV manufacturers to build to peak demand or build to a baseline, with surges being met by traditional drivers?

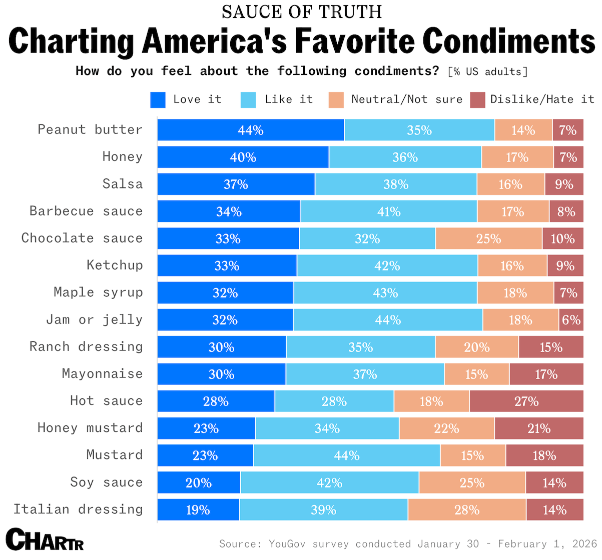

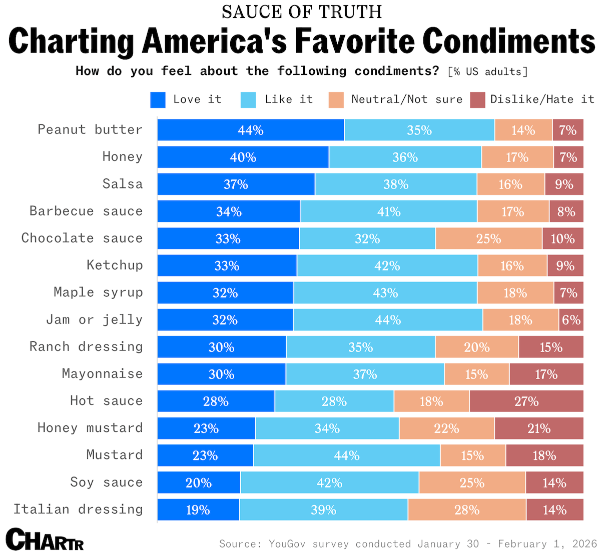

From Sherwood: Despite peanut butter ranking as America’s favorite condiment in a recent YouGov survey, ketchup remains the most ubiquitous, present in ~84% of U.S. households. The category is seeing renewed M&A activity, with Bachan’s acquired by The Marzetti Company and Tapatio by Highlander Partners

From ScreenRant: McDonald’s Valentine’s Day caviar-and-McNuggets kit crashed the company’s website and sold out instantly. Kits have resold on secondary marketplaces for as much as $600, for a bundle that includes a 1-ounce tin of caviar, crème fraîche, a mother-of-pearl spoon, and six nuggets that would set you back ~$100 retail.

From RestaurantDive: Sticking with McDonald’s, the company is rolling out craft sodas and energy drinks to the McCafé lineup after a “highly successful” 500-store test

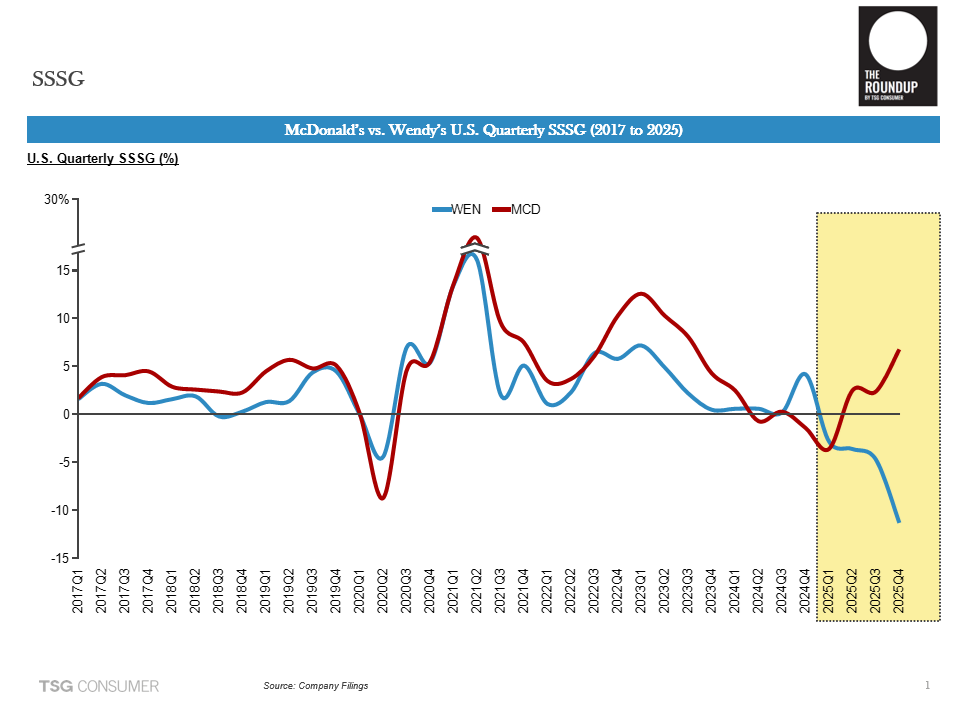

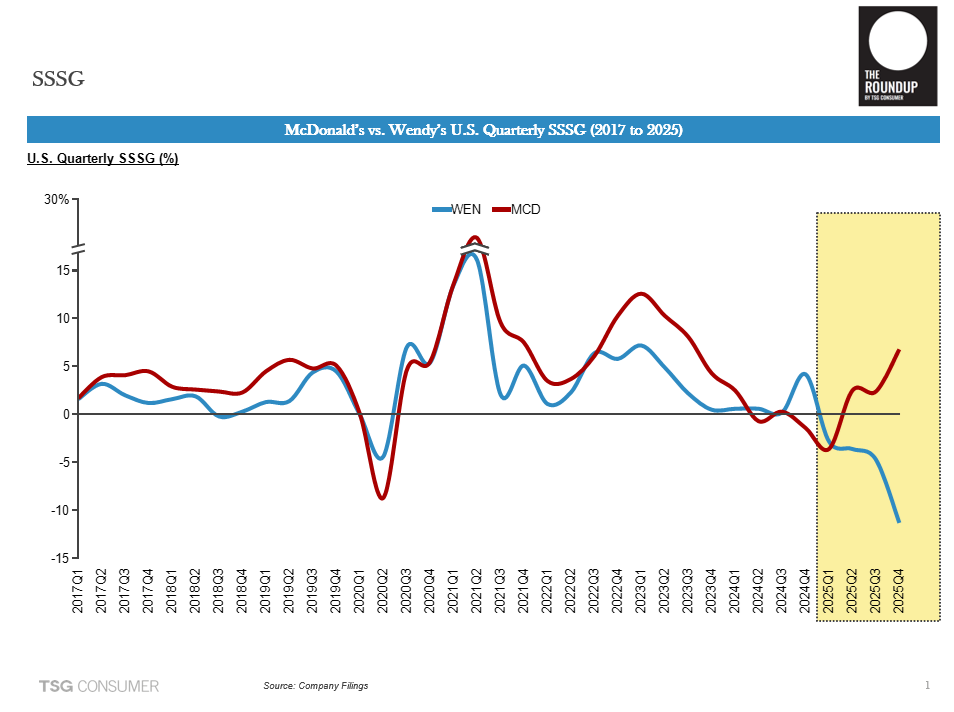

From Sherwood: Wendy’s had a brutal year capped by an even worse Q4, with SSSG of -11.3%. The previous low point was Q2 2020 at -4.4%, during COVID. Compared with McDonald’s recent performance, the contrast underscores how critical sustained innovation is to long-term SSSG